In the last year, the cost of energy has increased significantly. Gasoline, diesel, and domestic electricity and natural gas prices are now past the point that many people can bear. The problem affects businesses too, including manufacturing and agriculture, with consequences for the wider economy, jobs and the cost of living. It has led to a new word, “greenflation.” Greenflation is harming those who, literally, can least afford it.

However, instead of discerning what is behind these problems, what caused them, what role the federal government had and what it can do to ease the problem, the government is simply blaming others and pressing on. Treasury Secretary Janet Yellen is not only in denial but serially insists that the problem is that the administration just hasn’t proceeded on the “climate” front fast enough.

This is governmental malpractice. But the perpetrators are not without accomplices. The investor class, and big banks foremost among them, share equal responsibility. One of the chief culprits is a pernicious and destructive concept called Environmental, Social, and Governance investing.

Yellen: in "climate" denial.

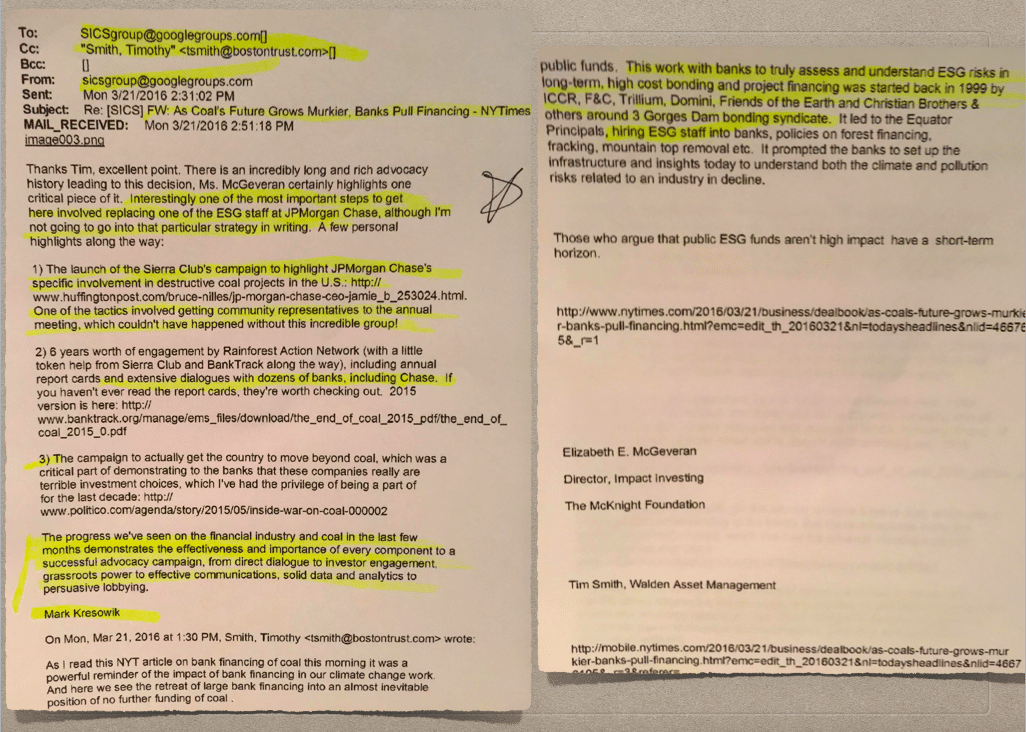

A 2016 email suggests that modern “ESG” began as anti-energy campaigning against financial institutions in 1999 focusing on hydropower, then morphed into anti-coal advocacy then soon expanded to opposing all abundant energy sources.

Bank of America seems to have been captured first, vowing to not finance hydrocarbon energy (beginning with coal). Freedom of Information Act litigation showed the bank's enthusiasm for the "climate" agenda. A senior bank official, Jim Mahoney, hired former Clinton hands as consultants to get the bank close to then-Secretary of State John Kerry with offers to sponsor as much of the 2015 Paris climate talks as it could.

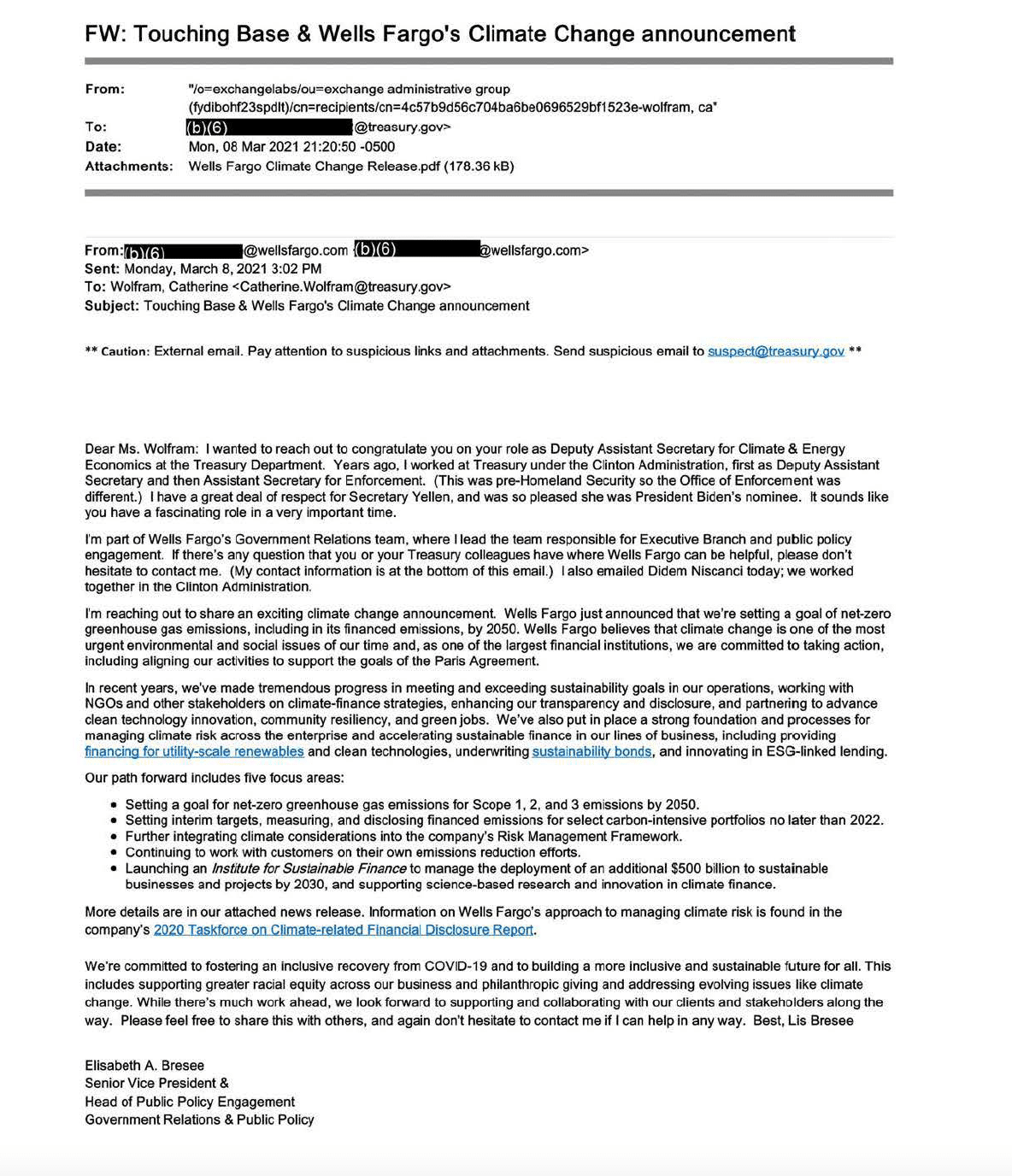

Yes, financial institutions sponsoring treaty negotiations. More recently, FOIA litigation produced still more craven correspondence, this time to Yellen from, among others, Wells Fargo. In a March 2021 email to a senior Treasury official, former Clinton Treasury official turned Wells lobbyist Elisabeth A. Bresee laid out the bank’s “climate” plan:

I'm reaching out to share an exciting climate change announcement. Wells Fargo just announced that we're setting a goal of net-zero greenhouse gas emissions, including in its financed emissions, by 2050. Wells Fargo believes that climate change is one of the most urgent environmental and social issues of our time and, as one of the largest financial institutions, we are committed to taking action, including aligning our activities to support the goals of the Paris Agreement.

In recent years, we've made tremendous progress in meeting and exceeding sustainability goals in our operations, working with NGOs and other stakeholders on climate-finance strategies, enhancing our transparency and disclosure, and partnering to advance clean technology innovation, community resiliency, and green jobs. We've also put in place a strong foundation and processes for managing climate risk across the enterprise and accelerating sustainable finance in our lines of business, including providing financing for utility-scale renewables and clean technologies, underwriting sustainability bonds. and innovating in ESG-linked lending.

Our path forward includes five focus areas:

The email closed by checking every box in the woke liturgy, about being—

committed to fostering an inclusive recovery from Covid-19 and to building a more inclusive and sustainable future for all.… includ[ing] supporting greater racial equity across our business and philanthropic giving and addressing evolving issues like climate change,” with a nod to the bank’s “clients and stakeholders.

This week, the bank announced it was demanding Paris-like emission cuts from companies it lends to.

This inherently conflicted, inane equivalence between and even preference for “stakeholders” (pressure groups and political interests) over shareholders and clients is, according to the Wall Street Journal, "using the ethical-custom concept to impose a progressive agenda on American businesses. It will have negative implications for investor returns.”

Yet the costs of this public-private tag-team are far greater. For example, in late 2021 some U.S. traditional energy producers, particularly coal and related industries (e.g., rail), were unable to affordably access capital markets to purchase (or, in some cases, re-purchase) equipment to ramp up production and transport in the face of a looming energy crisis (which continues today), leading to serious energy security concerns. The companies were informed by lenders that loaning money to, e.g., coal, gave the banks an “ESG problem.”

Wall Street, we have an ESG problem.

This resulted not from regulation but pressure campaigns including from a Biden administration that has made clear it has targeted hydrocarbon energy interests for extinction and that assisting them would not be well-received in Washington.

Such a policy directly threatens U.S. national security. The broader consequence of greenflation has pushed prices and the cost of living upwards, and destabilized manufacturing sectors in the U.S., U.K. and Europe. It has been a major contributor to European dependence on Russian energy, undermining the West’s geopolitical position and global security.

It has made firms worldwide increasingly dependent on China’s so-very-not-ESG manufacturing and materials. What this agenda demands of targeted industries is strongly contrary to America’s interests but is precisely as countries who wish us ill would have things.

Financial institutions draw from the same talent pool from which the Biden administration staffs itself, with the same woke priorities. This misguided partnership poses a grave danger to the U.S.

Article tags: Bank of America, banks, Biden Administration, ESG, greenflation, Janet Yellen, Wells Fargo

{kind=link}

{kind=link}

ESG has been around among oil producers for several years now. They have to address this to borrow money for field development. All of them borrow money from Wall Street.

This is nothing new.

There are more than two ways to approach the intent or outcomes of sustainable business practices. The "pros" often get tagged as left-leaning anti-industrialists and the "cons" often get tagged as head in the sand climate change deniers.

For the technically educated, measures to reduce carbon footprint include many sound technology advances that require financial commitment and truly result in efficiencies that improve the bottom line by reducing resource consumption such as energy, water and raw materials. The "sell" is to identify a sound framework of verifiable results that reduce bottom line and reduce social risks. The price tag for the latter is likely to far outweigh the price tag on the former in ways we don't even know right now.

The challenge in achieving lower bottom line is that benefits get transferred to investors and consumers and not just the select few in any one organization. The benefit is lower reliance on finite natural resources in the near term (think cost of resources) and lower risk in the long term (think and PFAS and water scarcity for the moment).

For sure there are benefits to lower carbon footprint. But with progress on this front, having a diverse range of choices for energy and extending the timeline for them can mitigate risk in the near and longer terms. There is a place in the economy for traditional fossil fuel energy sources to ensure financial security of nations so that investments in future opportunities for alternatives are not driven by "flick of the switch" thinking but by long range sound energy management.

There are more than two ways to approach the intent or outcomes of sustainable business practices. The "pros" often get tagged as left-leaning anti-industrialists and the "cons" often get tagged as head in the sand climate change deniers.

For the technically educated, measures to reduce carbon footprint include many sound technology advances that require financial commitment and truly result in efficiencies that improve the bottom line by reducing resource consumption such as energy, water and raw materials. The "sell" is to identify a sound framework of verifiable results that reduce bottom line and reduce social risks. The price tag for the latter is likely to far outweigh the price tag on the former in ways we don't even know right now.

The challenge in achieving lower bottom line is that benefits get transferred to investors and consumers and not just the select few in any one organization. The benefit is lower reliance on finite natural resources in the near term (think cost of resources) and lower risk in the long term (think and PFAS and water scarcity for the moment).

For sure there are benefits to lower carbon footprint. But with progress on this front, having a diverse range of choices for energy and extending the timeline for them can mitigate risk in the near and longer terms. There is a place in the economy for traditional fossil fuel energy sources to ensure financial security of nations so that investments in future opportunities for alternatives are not driven by "flick of the switch" thinking but by long range sound energy management.

The Biden-Harris Administration also wants to make ESG a valid criteria for ERISA purposes:

https://assets.realclear.com/files/2022/02/1965_realclear-erisa-ruperdarwall_feb_2022.pdf